Public Health·March 11, 2021

American Rescue Plan expands Obamacare subsidies, cutting premiums for millions

Enhanced subsidies cut marketplace premiums by $50 monthly, extending eligibility to middle-class families previously priced out

President Biden signed the American Rescue Plan Act into law on Mar. 11, 2021, as a $1.9 trillion COVID-19 relief package that included $34.2 billion over 10 years for enhanced Affordable Care Act premium tax credits. The law made two major changes: it eliminated the 400% federal poverty level income cap for subsidies (approximately $51,520 for individuals, $104,800 for families of four in 2021), and it reduced the premium contribution percentages at all income levels. For the first time, Americans earning above 400% FPL qualified for federal health insurance subsidies, with premiums capped at 8.5% of income.

The enhanced subsidies made dramatic differences for specific income groups

Americans with incomes between 100-150% FPL ($12,880-$19,320 for individuals in 2021) became eligible for $0 premium Silver plans

Those at 300% FPL saw their expected premium contribution fall from 9.83% of income to 6% A 60-year-old earning $55,000 annually (above the old 400% FPL cap) who previously paid full premium of approximately $958 monthly now paid only $385 monthly after subsidies—a 60% reduction Premiums decreased an average of $50 per person per month or $85 per policy per month across all enrollees.

The Congressional Budget Office projected the enhanced subsidies would prevent approximately 1.7 million Americans from becoming uninsured and estimated total costs of $22 billion in increased outlays and $12 billion in reduced revenue for fiscal years 2021-2030. The law also included a special provision for anyone receiving unemployment compensation in 2021, treating their income as no higher than 133% FPL to maximize subsidy eligibility. This meant unemployed workers could access nearly-free health coverage during the pandemic recession.

HealthCare.gov implemented the enhanced subsidies on Apr. 1, 2021, three weeks after Biden signed the law

The implementation required massive technical changes to the enrollment platform to recalculate subsidies for all income levels and remove the 400% FPL cap

Current enrollees had to return to the marketplace and update their applications to receive the new lower premiums starting May 1, 2021 Alternatively, they could wait and claim the additional premium tax credits when filing 2021 taxes in 2022, but this meant paying higher premiums throughout the year.

Congress passed the American Rescue Plan using budget reconciliation, which requires only 51 Senate votes and avoids Republican filibusters but limits legislation to provisions affecting federal spending and revenue

The Byrd Rule prohibits extraneous provisions in reconciliation bills, forcing Democrats to make the enhanced subsidies temporary (tax years 2021-2022 only) rather than permanent

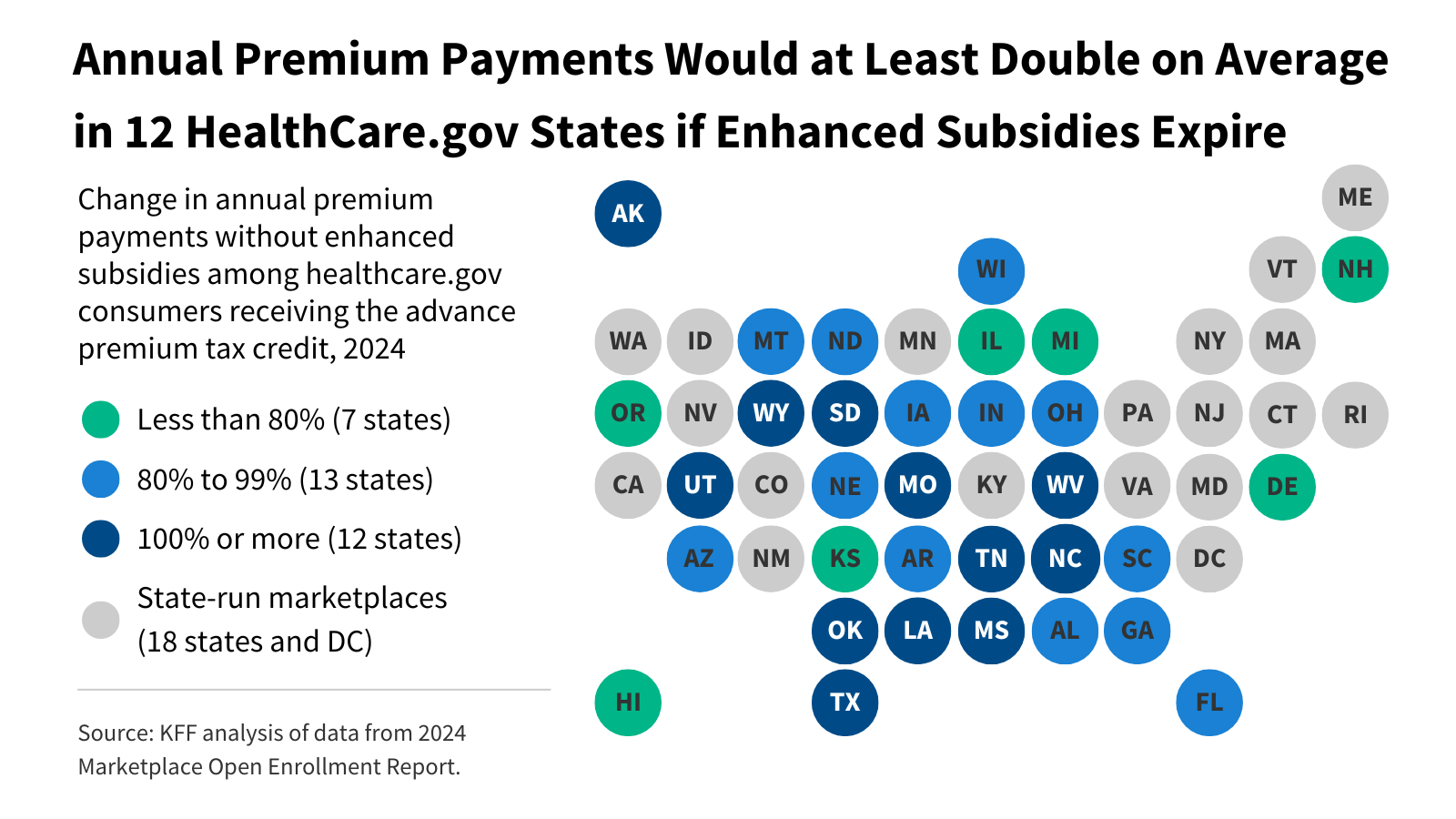

This created ongoing political fights over extension The Inflation Reduction Act later extended the subsidies through 2025, but they expired Dec. 31, 2025, triggering the current premium crisis.

Marketplace enrollment reached 12 million Americans for 2022 coverage—the highest enrollment since 2016 and up from 8.3 million in 2021

State-based marketplaces saw even larger gains: California's Covered California added state subsidies on top of federal ones, making coverage nearly free for many lower-income residents

Combined federal and state subsidies created $0 or near-$0 premiums for families earning up to 400% FPL in states like California, Colorado, and New York The 12 states that hadn't expanded Medicaid saw smaller enrollment gains because their poorest residents remained in the coverage gap.

Republicans uniformly opposed the American Rescue Plan, with zero Republican votes in either chamber

They argued enhanced subsidies were too expensive, would encourage people to drop employer coverage for subsidized marketplace plans, and represented federal overreach into healthcare markets

They predicted premium increases and market instability Democrats countered that employer coverage was eroding anyway, premiums were already rising, and enhanced subsidies prevented emergency room overuse and reduced uncompensated care costs for hospitals The partisan divide continues today as enhanced subsidies face expiration.

The temporary nature of enhanced subsidies created market uncertainty for insurers setting rates for future years

Insurance companies must submit rate filings in spring for coverage beginning the following Jan., meaning they set 2023 rates in spring 2022 without knowing if Congress would extend subsidies beyond Dec. 31, 2022

Some insurers priced in subsidy expiration with higher rates, while others assumed extension This uncertainty persists: insurers set 2026 rates in spring 2025 expecting subsidy expiration, leading to the current crisis where premiums are set to more than double for 22 million Americans.

Related Topics

3

Enhanced ACA premium tax credits expire, millions face cost hikes

9 million enrollees face doubled premiums as congressional gridlock ends enhanced subsidies

Inflation Reduction Act extends enhanced Obamacare subsidies through 2025

Congress extends temporary subsidies preventing $800 annual premium spike for 13 million enrollees

ACA subsidies expire after Senate fails to act on shutdown deal

Congress punts healthcare fight until after deadline, leaving millions facing premium spikes

19 questions

Start the review