Digital RightsEconomyTechnology

July 21, 2025Banking groups warn stablecoins could drain trillions in deposits under GENIUS Act

ABA warns GENIUS Act loophole threatens $6.6T in bank deposits

President Trump signed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins) on July 18, 2025, creating the first federal regulatory framework for payment stablecoins. The Senate passed it 68-30 on June 17, 2025, with 17 Democrats joining all 51 Republicans. The House passed it 308-122 on July 17, 2025. The law covers issuers with more than $10 billion in outstanding stablecoins and creates two licensing tracks: a federal OCC charter for nonbank issuers or existing banking regulatory oversight for bank-affiliated issuers. Circle (USDC) and Tether (USDT) together controlled roughly 82% of the $260+ billion stablecoin market as of mid-2025.

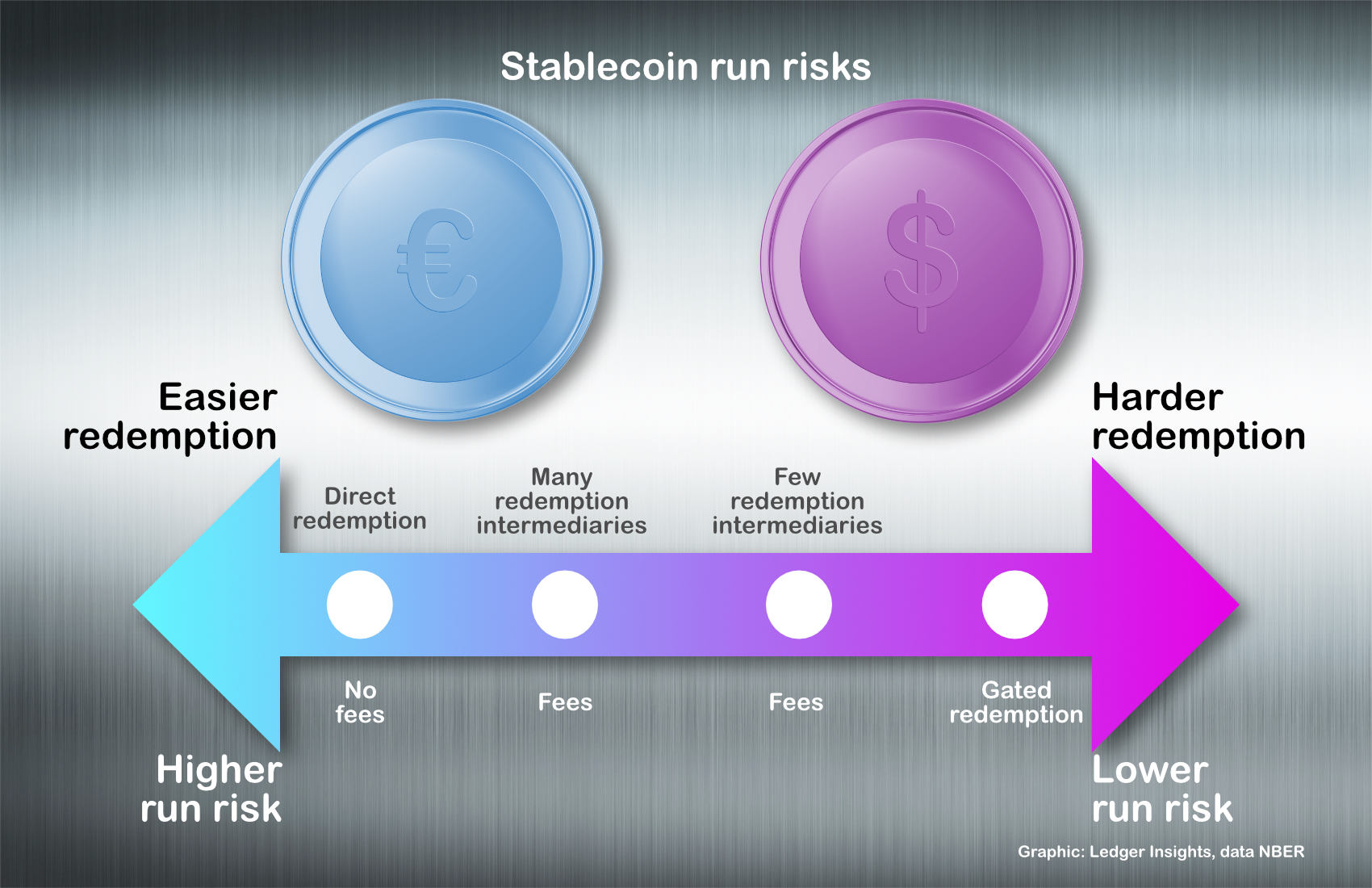

The GENIUS Act requires stablecoin issuers to hold 100% reserves in U.S. dollars, Treasury bills, or similarly liquid assets; publish monthly disclosures of reserve composition; and prioritize stablecoin holders' claims over all other creditors in bankruptcy. Section 4(a)(11) explicitly bans issuers from paying any form of interest, yield, tokens, or other consideration to stablecoin holders. Banking groups welcomed the reserve requirements but immediately identified a loophole: the prohibition covers issuers — entities like Circle that create the stablecoin — but not exchanges or affiliated platforms that distribute it.

The American Bankers Association and 52 state banking associations sent a joint letter to Congress in December 2025 urging lawmakers to close the affiliated-yield loophole. The letter warned that platforms like Coinbase — offering 4.1% annual yield on USDC as of August 2025 — and PayPal, offering 3.7% on PYUSD, were exploiting the gap. Independent Community Bankers of America President Rebeca Rainey called on Congress to amend the GENIUS Act before platforms could 'disintermediate core banking activity, including deposit-taking and lending, which harms local communities.'

The Treasury Borrowing Advisory Committee estimated in April 2025 that yield-bearing stablecoins could trigger up to $6.6 trillion in bank deposit outflows — conditional on stablecoin platforms being able to offer interest. Bank Policy Institute research found that for every $100 billion in net deposits leaving banks for stablecoins and not recycled back into the banking system, bank lending contracts by $60 to $126 billion, depending on conditions. Traditional banks hold approximately $18 trillion in deposits and use them to fund mortgages, small business loans, and farm credit.

Community banks face the steepest competitive risk. Unlike large banks, which can access wholesale capital markets and offer stablecoin custody services as new revenue, community banks rely almost exclusively on local retail deposits for their lending capacity. Roughly 4,800 community banks serve rural counties, small towns, and low-income markets that larger institutions don't find profitable. A March 2023 precedent illustrated the systemic exposure: when Silicon Valley Bank failed, Circle held $3.3 billion in USDC reserves at SVB — only $250,000 of which was FDIC-insured. USDC fell to $0.87 on secondary markets before the government backstop restored confidence.

The GENIUS Act's 100% reserve requirement creates structural demand for U.S. Treasury securities: every dollar of stablecoin outstanding requires a dollar held in Treasuries or equivalent assets. Treasury Secretary Scott Bessent publicly framed this as a strategic benefit, calling stablecoins 'an important tool for maintaining dollar dominance and ensuring demand for U.S. Treasuries.' The Trump administration's support for the GENIUS Act despite banking industry opposition reflects this geopolitical calculation — reducing Treasury borrowing costs by creating hundreds of billions in new institutional demand for short-term U.S. government debt.

Tether, the issuer of USDT with $173 billion in market cap as of late 2025, faces the most compliance pressure from the GENIUS Act. Tether is registered in the British Virgin Islands and paid $41 million in CFTC penalties in 2021 for misrepresenting its reserves — the regulator found that Tether only held fully-backed dollar reserves on 27.6% of days in a 26-month sample period. The GENIUS Act bans foreign entities from issuing regulated stablecoins in the U.S. market and gives foreign issuers a two-year transition period to obtain U.S. licensing or exit. If Tether exits, Circle's USDC would capture most of the dollar stablecoin market by default.

Sen. Elizabeth Warren (D-MA) voted against the GENIUS Act, arguing the law 'massively expands the marketplace for stablecoins while failing to address basic national security risks.' Her floor speech cited Treasury Department data showing that stablecoins accounted for more than 60% of all illicit crypto transactions, making them a preferred payment mechanism for sanctions evaders and money launderers. She also highlighted that the law creates a conflict of interest: President Trump's own USD1 stablecoin — backed by a firm with ties to Abu Dhabi investors — would now be regulated under a framework he signed into law.

Related Topics

2

25 questions

Start the review